How One Credit Card Interest Charges Calculated?

By OneCard | February 03, 2021

In an earlier post, we had provided a guide to understanding your OneCard statement, as well as various terms and components in it. In this post, we explain in greater detail how interest is charged on your OneCard - and how you can avoid paying it 😉

Table of contents:

- Understanding One Credit Card Statement

- What is Credit Card Interest Rate?

- How OneCard Interest Rate Is Calculated?

- When is interest charged?

- Is there any interest-free period to repay card dues?

- Is paying just the Minimum Amount Due sufficient?

- How is the refund received (if any) adjusted from the outstanding amount?

- Is it possible to avoid paying any interest charges at all?

- FAQs

Understanding One Credit Card Statement

To quickly recap, your OneCard statement is generated every month, and displays your spends made in that month, along with any credits (refunds, chargebacks, or spends repaid with points). The statement also mentions the Total Amount Due and Minimum Amount Due, and a date by when a payment must be done.

The Total Amount Due (TAD) is the overall amount due on your card when the statement is generated, and Minimum Amount Due (MAD) is the amount you must repay by the Payment Due Date (PDD) to keep your OneCard account in good standing. Minimum amount due is usually 5% of (Fees+Interest+Purchases+GST) + 100% of EMI posted +100% of Overlimit spends . Check out our previous post about understanding your OneCard statement.

What is Credit Card Interest Rate?

All credit card accounts are subject to a standard interest rate called the Annual Percentage Rate (APR). While it is expressed for a year, it is generally shown on a monthly basis for easier understanding.

How OneCard Interest Rate Is Calculated?

At the end of each day, the current balance/outstanding amount will be multiplied by the daily rate to arrive at the daily interest charges, which then get added to your outstanding balance. A simple formula would be as below: ((Number of days X Entire outstanding amount X (Interest rate per month x 12 months))/365 days.

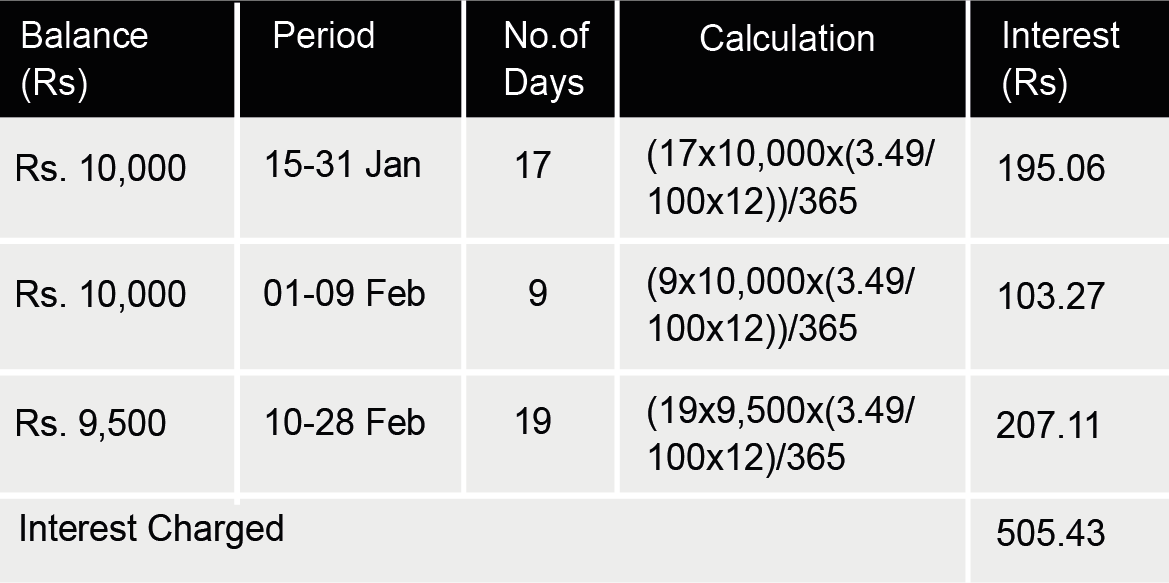

Sample Illustration 1 (dues not paid in full)*

Purchase: Rs.10,000 on January 15, 2021

Statement Date: February 01, 2021

Total Amount Due: Rs.10,000

Payment Due Date: February 18, 2021

Payment Done: Rs. 500 on February 10, 2021

No other transactions in February.

As per the formula shared above, the interest will be charged as follows:

Goods & Services Tax (GST) at the prevailing rate (currently 18%) will be levied on this interest charged, which is Rs. 90.98.

This will be added to the outstanding amount so in your statement on March 01, 2021, the Total Amount Due will be Rs.10,096.41 (Rs.9,500 + Rs. 505.43 + Rs.90.98)

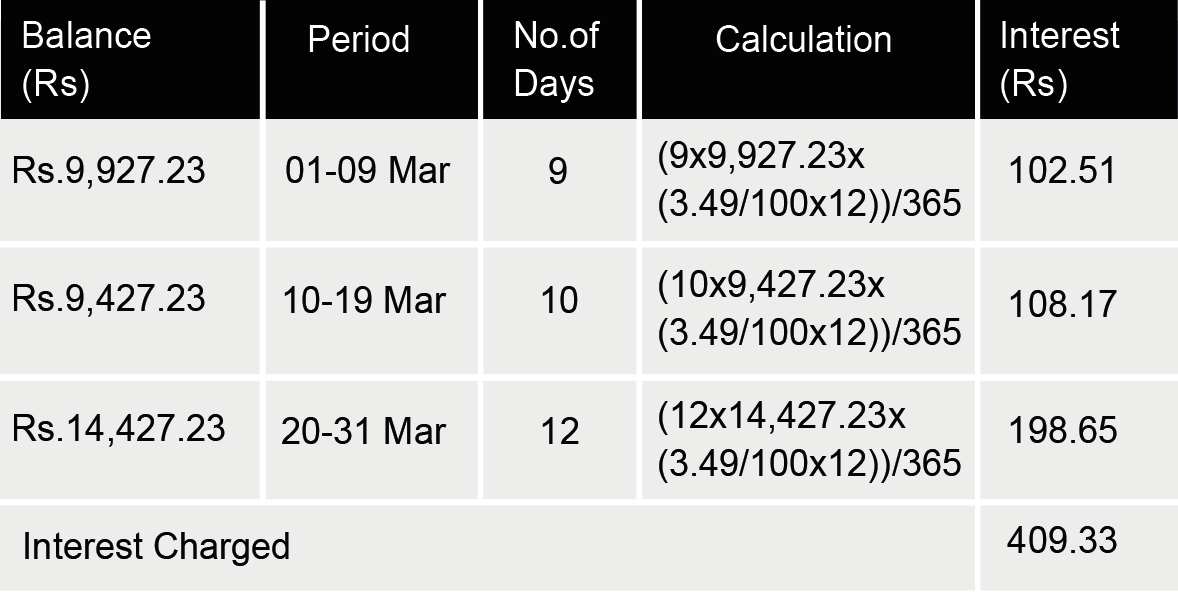

Sample Illustration 2 (Dues revolved, fresh purchase)*

Statement Date: March 01, 2021

Total Amount Due: Rs.9,927.23

Payment Due Date: March 18, 2021

Payment Done: Rs. 500 on March 10, 2021

New Purchase: Rs.5,000 on March 20, 2021

Interest will be charged as follows:

Goods & Services Tax (GST) at the prevailing rate (currently 18%) will be levied on this interest charged, which is Rs.73.68.

This will be added to the outstanding amount so in your statement on April 01, 2020, the Total Amount Due will be Rs.14,910.24 (Rs.14,427.23 + Rs. 409.33 + Rs.73.68).

* These illustrations are meant to be indicative and to show how interest is calculated and charged. Actual amounts can vary depending on specific cases.

Additional read: What is Credit Card Billing Cycle and How Does it Work?

When is interest charged?

When you spend on a credit card, you are doing so with money that is borrowed from the bank or financial institution. If you repay the Total Amount Due within the due date, no interest is applicable. However, there are other situations when interest would be charged, such as:

a) When you fail to pay the outstanding dues within the due date

If you don’t pay your OneCard dues at all, interest will be charged on this outstanding amount as well as on new purchases after the due date, till the dues are repaid. A Late Payment Charge (LPC) will also be levied. Non-payment will lead to your account being reported to credit bureaus as delinquent and this will impact your credit score and overall creditworthiness.

b) When the repayment amount is even lesser than the Minimum Amount Due

This is an unwanted situation and you should avoid it at all costs, as it is equivalent to making no payment at all. It can cause your account to be reported to credit bureaus as delinquent. It can also affect your credit score besides levy of charges and fees.

c) When you pay only the Minimum Amount Due by the due date

Repaying only the Minimum Amount Due will help you avoid Late Payment Charges. However, interest will be charged on the balance amount payable as well as on all new purchases after the due date.

d) When you pay more than Minimum Amount Due but less than Total Amount Due

If you keep paying an ad-hoc amount higher than Minimum Amount Due but less than the Total Amount Due, the interest charges keep accumulating - not just on your outstanding balance each month but on every subsequent purchase you make.

e) When you use your OneCard to withdraw cash from an ATM*

* This functionality is currently disabled for all cardmembers

Is there any interest-free period to repay card dues?

Your OneCard has an “interest-free” period of 48 days. What this means is: if you do not have any prior outstanding dues on your card and make a purchase, you get a grace period to repay these purchases without incurring any interest charges.

If you get your OneCard statement for December 2020 on January 01, 2021 and make a purchase the same day, you can repay this amount by February 18, 2021 - giving you a grace period of 48 days, and allowing you to enjoy credit at zero interest. This grace period will vary depending on your date of purchase.

However, if you have outstanding dues from the previous statement, there is no grace period allowed and interest will be charged on all fresh purchases, till dues are cleared completely.

Is paying just the Minimum Amount Due sufficient?

While paying just the Minimum Amount Due (MAD) by the payment date will keep your account in good standing and avoid Late Payment Charges (LPC), you should keep in mind that the entire unpaid balance will begin attracting interest along with ALL fresh purchases you make - there will be no grace period applicable in such cases.

Repaying just the Minimum Amount Due every month is also known as “revolving credit” and can lead you into a debt trap. Depending on the overdue amount and fresh purchases, it can even take up to 5-10 years to clear all dues. Use this option only if you are going through a financial crisis and cannot make higher repayments.

This will also impact your credit score, as credit utilisation ratio (how much credit you’ve used up) is an important factor. This ratio will continue to be high if you keep repaying only the minimum amount due each month.

💡 Tip: Always aim to pay the entire outstanding amount by the due date. You can also try to repay an amount higher than the Minimum Amount Due. This will not only reduce your debt faster but also free up your credit limit. Do note that interest charges will keep accumulating, so use this option sparingly.

How is the refund received (if any) adjusted from the outstanding amount?

If any refund is received by you against any previous purchase on your OneCard then it is automatically adjusted against your billed outstanding amount.

Is it possible to avoid paying any interest charges at all?

Yes, very much! The easiest way to avoid paying any interest charges is to pay the Total Amount Due as per your statement before the Payment Due Date. 😎

FAQs

1. What are the standard credit card interest charges for OneCard?

Interest rates on credit cards usually ranges from 2.5% to 3.5% per month. The interest charge for One Credit Card is 3.75% per month.

2. How can I avoid interest charges on my OneCard?

You can avoid interest charges on your One Credit Card by paying your credit card bill on time and in full each month.

3. How are OneCard late payment charges calculated?

One Credit Card late payment charges vary based on your total outstanding amount and can be up to ₹1,250.

4. Is credit card interest charged daily?

Yes, most credit card issuers calculate and compound interest daily.

**Disclaimer: The information provided in this webpage does not, and is not intended to, constitute any kind of advice; instead, all the information available here is for general informational purposes only. FPL Technologies Private Limited and the author shall not be responsible for any direct/indirect/damages/loss incurred by the reader for making any decision based on the contents and information. Please consult your advisor before making any decision.

Sharing is caring 😉